Procedure for bringing appeals against decisions made by the tax administrator and for submitting appeals to the State Tax Inspectorate

Procedure for bringing appeals against decisions made by the tax administrator and for submitting appeals to the State Tax Inspectorate

The State Tax Inspectorate examines two types of disputes - tax disputes and other disputes.

TAX DISPUTES

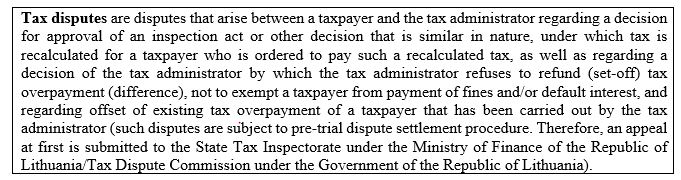

Tax disputes are examined in accordance with the procedure set out in Chapter IX of the Law of the Republic of Lithuania on Tax Administration (hereinafter - the LTA):

1) if a decision has been made by the County State Tax Inspectorate (hereinafter – the CSTI), an appeal may be brought against it not later than within 20 (twenty) days from the date of service of this decision to a taxpayer to the State Tax Inspectorate under the Ministry of Finance of the Republic of Lithuania (hereinafter – the STI under the Ministry of Finance; address Vasario 16-sios str. 14, 01514 Vilnius through the CSTI that has made the decision (addresses of the CSTI are available publicly on the website of the State Tax Inspectorate at www.vmi.lt/cms/aptarnavimo-skyriai);

An appeal against a decision of the STI under the Ministry of Finance regarding tax dispute, that has been made during examination under the pre-trial procedure of an appeal regarding a relevant decision of the CSTI specified above, may brought under the procedure set out in Chapter IX of the LTA not later than within 20 (twenty) days from the date of service of this decision to a taxpayer by submitting an appeal optionally: to the Tax Dispute Commission under the Government of the Republic of Lithuania (Vilniaus str. 27, 01402 Vilnius) by submitting an appeal through the STI under the Ministry of Finance (Vasario 16-sios str. 14, 01514 Vilnius), or to Vilnius Regional Administrative Court (Žygimantų str. 2, 01102 Vilnius).

2) if a decision has been made by the STI under the Ministry of Finance, an appeal may brought against it not later than within 20 (twenty) days from the date of service of this decision to a taxpayer to the Tax Dispute Commission under the Government of the Republic of Lithuania (Vilniaus str. 27, 01402 Vilnius) by submitting an appeal through the STI under the Ministry of Finance (Vasario 16-sios str. 14, 01514 Vilnius).

OTHER DISPUTES

Bringing appeals against decisions of the CSTI, where appealing against such decisions could result in other (non-tax) dispute (there can be dispute regarding taxes but when dispute is non-tax dispute).

Other disputes are examined under the procedure prescribed by the Law of the Republic of Lithuania on the Procedure for Pre-Trial Examination of Administrative Disputes and/or by the Law of the Republic of Lithuania on Administrative Proceedings (hereinafter – the LAP).

If a decision has been made by the CSTI, an appeal may be brought against it not later than within 1 (one) month from the date of service of this decision by submitting an appeal optionally: to the Lithuanian Administrative Disputes Commission (when an appeal is brought against a decision made by Vilnius CSTI) or to its territorial subdivision (when an appeal is brought against a decision made by other CSTI (not Vilnius CSTI) located in the territory of activity of the relevant CSTI or to the regional administrative court (to Vilnius Regional Administrative Court (when an appeal is brought against a decision made by Vilnius CSTI) or to the relevant chamber of the Regional Administrative Court (when an appeal is brought against a decision made by other CSTI (not Vilnius CSTI)) in whose territory of activity the registered office of the CSTI, that has made that decision, is located, i.e.:

If a decision has been made by the CSTI:

1) if a decision has been made by Vilnius CSTI – an appeal has to be submitted to Lithuanian Administrative Disputes Commission (Vilniaus str. 27, 01402 Vilnius) or to Vilnius Regional Administrative Court (Žygimantų str. 2, 01102 Vilnius);

2) if a decision has been made by Kaunas CSTI - an appeal has to be submitted to Kaunas Regional Division of Lithuanian Administrative Disputes Commission (Laisvės ave. 36, 44240 Kaunas) or to Regional Administrative Court, Chamber of Kaunas (A. Mickevičiaus str. 8 A, 44312 Kaunas);

3) if a decision has been made by Klaipėda CSTI - an appeal has to be submitted to Klaipėda Regional Division of Lithuanian Administrative Disputes Commission (Manto str. 37, 92236 Klaipėda) or to Regional Administrative Court, Chamber of Klaipėda (Galinio Pylimo str. 9, 91230 Klaipėda);

4) if a decision has been made by Panevėžys CSTI - an appeal has to be submitted to Panevėžys Regional Division of Lithuanian Administrative Disputes Commission (Respublikos str. 62, 35158 Panevėžys) or to Regional Administrative Court, Chamber of Panevėžys (Respublikos str. 62, 35158 Panevėžys);

5) if a decision has been made by Šiauliai CSTI - an appeal has to be submitted to Šiauliai Regional Division of Lithuanian Administrative Disputes Commission (Dvaro str. 81, 76299 Šiauliai) or to

If a decision has been made by the STI under the Ministry of Finance:

If a decision has been made by the STI under the Ministry of Finance, an appeal may be brought against it not later than within 1 (one) month from the date of service of this decision by bringing an appeal optionally to Lithuanian Tax Dispute Commission (Vilniaus str. 27, 01402 Vilnius) or to Vilnius Regional Administrative Court (Žygimantų str. 2, 01102 Vilnius).

Attention: bringing an appeal against documents of a recommendatory / informative / explanatory nature!

A person has the right to apply to an administrative court only for individual legal acts, adopted in the field of public administration, that produce legal effects on a person, i.e. affecting the rights of persons or the interests protected by law. Relevant documents of the tax administrator, which are procedural / intermediate, and which in themselves do not affect the legal status of a taxpayer, cannot be an independent subject of an administrative case.

The following elements are considered not to be subject to appeal brought before the administrative court: certificate of operational inspection; a decision to extend the term for the examination of an appeal regarding a tax dispute; instruction to the taxpayer to provide documents, explanations, information on sources of acquisition of property and (or) receipt of income; to provide additional documents regarding the conclusion of a tax loan; an information notice to a taxpayer stating the basis on which tax arrears have been calculated; notice to a taxpayer on deficiencies identified and a request to eliminate them; information notice on the payment of current contributions to the company being restructured; etc.

LEGAL INFORMATION

Law of the Republic of Lithuania on Public Administration.

Law of the Republic of Lithuania on Administrative Proceedings.

Law of the Republic of Lithuania on Tax Administration.

Taxpayers may also make complaints regarding the legal acts adopted by the STI, as well as regarding the legality of the respective actions (omissions) in accordance with the Law of the Republic of Lithuania on Public Administration (hereinafter – the LPA), the Rules for Examination of Applications Submitted by Individuals and Services Provided to Them in Public Administration Institutions, Agencies and Other Public Administration Entities approved by the Resolution No 875 of the Government of the Republic of Lithuania of 22 August 2007 on the Approval of the Rules for Examination of Applications Submitted by Individuals and Services Provided to Them in Public Administration Institutions, Agencies and Other Public Administration Entities, and the Rules for Personal Service at the State Tax Inspectorate approved by the Order No VA-77 of the State Tax Inspectorate under the Ministry of Finance of the Republic of Lithuania of 17 December 2007 on the Approval of the Rules for Personal Service at the State Tax Inspectorate.

Complaints are dealt with under the administrative procedure within 20 working days of its commencement (according to new version of the LPA taking effect from 1 November, 2020- from the day of receiving the complaint). Complaints may be made by post or electronic means. Complaints made by electronic means must contain an electronic signature identifying the complainant.